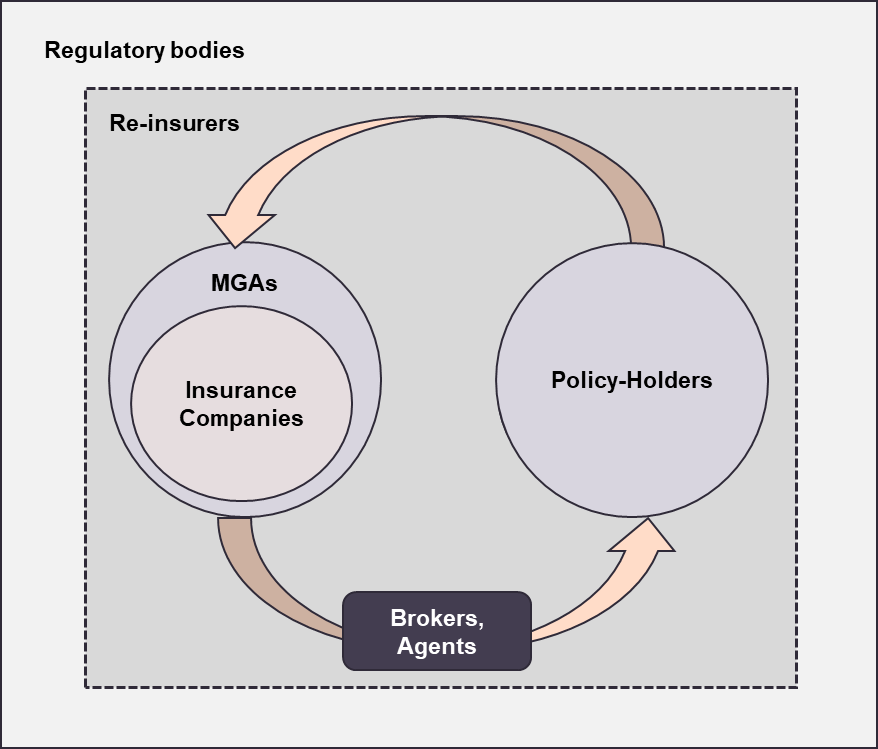

The insurance industry is a complex ecosystem that plays a crucial role in our modern economy, offering financial protection and peace of mind to individuals and businesses. To best understand this space, picture a teeming marketplace where risks are bought and sold:

- On one side, we have insurance companies (the risk takers) that range from century-old giants such as Allianz and AXA to leaner challenger providers (i.e. Lemonade, Hippo) attempting to disrupt the status quo with technology

- On the other side we have policy holders encompassing individuals and businesses looking to protect themselves from life’s uncertainties

- Reinsurers sit behind the scenes and can be defined as the insurance companies for insurance companies. They mainly provide insurers with a way to spread their risk and allow them to take on large policies and more diverse portfolios by “ceding premiums” to reinsurers

- Insurance companies and policy holders are bridged by brokers and agents who assist with distribution of policies, serving as the friendly faces in front of customers, helping them navigate the confusing fine print

- MGAs (Managing General Agents) are a specialized type of intermediary that are granted more authority than typical agents & brokers with their role extending to a much broader set of functions such as underwriting, policy issuance and claims management and essentially being the “front-end” to the customer experience

The existence of insurance can be traced back to the 18th century, and while it has considerably evolved over time, insurance companies have been famously resistant and slow towards the adoption of technology. Key challenges include:

The existence of insurance can be traced back to the 18th century, and while it has considerably evolved over time, insurance companies have been famously resistant and slow towards the adoption of technology. Key challenges include:

- Reliance on outdated legacy systems: Mission-critical, sticky platforms that are ****difficult and expensive to integrate with newer technologies

- Stringent regulatory compliance: Highly regulated nature of the insurance industry creates considerable hurdles for digital transformation

- Complicated customer journeys: Fragmented nature of customer-insurer interactions makes it difficult to provide seamless E2E digital experiences

- Natural risk aversion: Highly conservative nature of the industry implies significant hesitation across the board to invest in new technologies

- Data quality issues: Poor data quality in siloed systems and questionable sophistication of data collection methods slows down digital initiatives

As such, the prevalent struggle experienced in the Insurtech space is well-justified, and after a hope-inducing period fueled by a boom of VC funding and exits between 2019-2021, the hype seems to have partially subsided. Nonetheless, several trends (i.e. customers expecting digital experiences, increasing quantity & quality of data, desire for tailored experiences etc…) paired with the astounding leaps made in AI, keep the door ajar for Insurtech to rebound. While a full disruption of the insurance market as a whole remains unlikely today, we see certain critical links of the insurance value chain well positioned to considerably benefit from the implementation of AI.

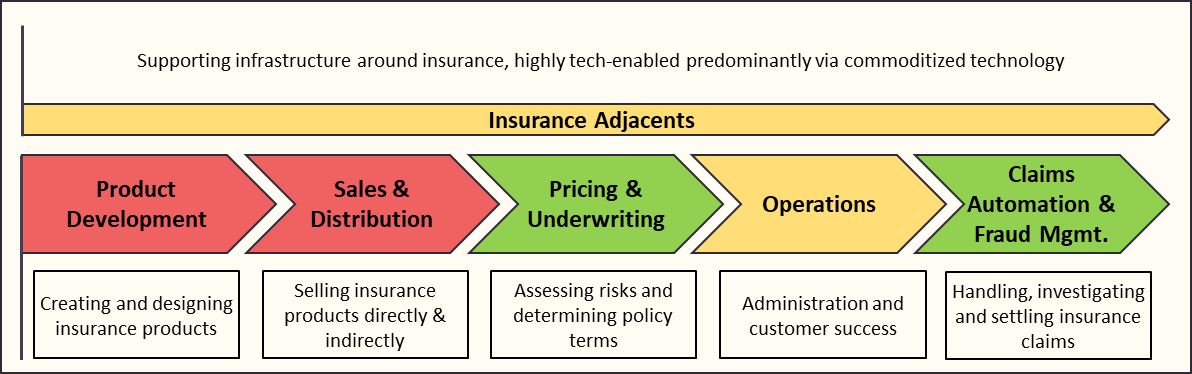

1. Insurtech in the Modern Enterprise: Identifying opportunities within the Carrier Value Chain

Advanced data science and AI has the potential of accelerating the adoption of insurance technology by carriers. Given the historical resistance and frictions towards adoption, technology will likely be embraced progressively, starting with areas of the value chain where digitalization can yield the most impact and fastest time to value.

The carrier value chain can be segmented as follows:

1.1 Product Development

Insurance companies go through rigorous product development processes, involving (among many other things) considerable market research, brainstorming, customer analysis, prototyping and testing. While technology can assist at various stages of the process, there don’t seem to be any transformational applications that would convince large insurers to entirely overhaul their product development process (toggle for examples).

- Using advanced analytics and AI to analyze immense datasets, enabling better understanding of customer needs and the creation of tailored products

- Customer journey mapping solutions to help insurers identify and alleviate existing pain points to improve product offerings

- Project management solutions to help streamline and coordinate the various parties and processes involved in product development

- Using AI-based models to help assess customer needs, preferences and behaviors to improve product customization

- Challenger insurances (i.e. Lemonade, Hippo) developing and underwriting their own insurance products in underserved segments such as pet insurance

1.2 Sales & Distribution

There have been considerable innovative attempts at disrupting the insurance distribution process that generated a lot of excitement, but few tech-enabled actors have stood the test of time. The rise of AI and Agentic AI have the potential of helping here and several start-ups are taking advantage of this, but the fragmented nature of the distribution function in insurance makes it difficult to fully centralize and streamline (toggle for a deeper dive).

- The first wave consisted of digital marketplaces partnering with large carriers to provide a centralized and quick purchasing experience (i.e. Next Insurance, Policygenius, GoHealth). This brought to light the daunting nature of insurance procurement and the importance of intermediaries to assist buyers

- The second wave is more promising with AI and agentic functionalities providing customers with AI-enabled guidance (i.e. Agentero, Zelros, AgentSync)

- Other technologies such as digital marketing and predictive analytics also play key roles within sales and distribution

- We must also mention embedded insurance as a promising tech-enabled means of distribution but suffers from the same bottlenecks as distribution platforms

1.3 Pricing & Underwriting

Pricing and underwriting are mission-critical activities for any insurance company. These processes are highly complex, technical, data driven and high-stakes, with limited room for error. It is therefore widely accepted that the prospect of using AI for policy pricing and underwriting is highly promising and most large carriers are actively exploring the prospect of using the technology as a core pillar. While several startups have been gaining traction, several carriers to build to minimize friction with legacy systems, rely on their own models and talent and avoid data privacy concerns. Nonetheless, the potential benefits are numerous:

- Enhanced Risk Assessment: AI-powered systems can analyze vast amounts of data from various sources to create more comprehensive risk profiles quicker, more accurately and in real-time. This in turn, allows insurers to offer more tailored policies with potentially lower premiums and greater flexibility.

- Improved Efficiency: AI models can process and analyze data countless times faster than traditional methods, enabling near real-time risk assessment. This allows insurers to perform more granular and frequent risk assessments, resulting in faster responses to customers and more personalized policies. In fact, certain early-adopting carriers saw a 90% reduction time for risk assessment and 25% increase in the accuracy of risk predictions (Avenga).

- Personalized Pricing: As covered above, AI improves and enables insurers to conduct enhanced data analysis, which in turn enables real-time risk assessment, ultimately informing pricing. This brings to light the possibility of introducing personalized and dynamic pricing. This allows insurers to make real-time adjustments to premiums based on individual customer data, market trends and competitive forces, ensuring that pricing remains competitive and reflective of real-life risk factors. Furthermore, AI algorithms can (on the basis of historical data) forecast future risks and claim probabilities, enabling further tailoring of prices.

- Example 1: Auto insurance premiums could be recalculated weekly/monthly on the basis of driving patterns tracked through telematics devices (see also telematic insurance 3.5)

- Example 2: Agri-insurance premiums recalculated periodically on the basis of data captured by soil-sensors monitoring its evolving condition (see also parametric insurance 3.5)

While the use of AI is highly promising when it comes to pricing and underwriting, its usage is significantly dependent on the quality of underlying data, a bottleneck that insurers have been famously poor at addressing. This is primarily due to data disparity across multiple and siloed legacy systems. As such, before any adoption can realistically take place at scale, insurers need to work on the quality of their data stack to formally become AI-ready.

Start-up Examples:

| Company Name | Description | HQ | Last Round | Total Raised ($M) | Invested Funds |

|---|---|---|---|---|---|

| Akur8 | AI-Pricing | France | Series C | 195 | OnePeak, Hedosophia, Guidewire |

| Concirrus | AI-Pricing | UK | Series B | 50 | CommerzVentures, IQ Capital Partners |

| Hyperexponential | AI-pricing | UK | Series B | 88 | A16Z, Highland Europe, Battery Ventures |

| Archipelago | Risk Assessment | Netherlands | Series B | 73 | Scale Venture Partners, Stone Point Capital |

| Artificial Labs | AI-pricing | UK | Series A | 31 | Mundi, Force over Mass, TrueSight Ventures |

| CyberCube | Risk Assessment | USA | Series C | 105 | Stone Point Capital, Morgan Stanley |

| Roots Automation | AI-pricing | USA | Series B | 44 | CRV, Harbert Growth Partners |

1.4 Operations

Operations refer to the day-to-day administrative and customer success activities of an insurance carrier. This encompasses (among many other things) policy management, customer service, data management, compliance, reporting and administrative support. While technology has played a key role here for a while, most activities are well served by legacy ERPs and the most obvious applications of AI involve using agentic capabilities to enhance efficiency and customer experience. Nonetheless, operations remain a central pillar to the proper functioning of a large carrier making the segment tough to penetrate:

- Relatively high technology adoption for the management of administrative activities such as policy management, data management, compliance, reporting and administrative support with success stories such as Guidewire. Mainly served by legacy ERPs although certain vertical startups (i.e. Briteco, Element, Genasys) attempt to cater to certain insurance-specific tasks. Agentic AI platforms can also be leveraged to streamline certain processes (Kore.ai, Roots Automation, Agentero, Druid, DeepOpinion/Otera)

- Customer Success, specifically for renewal management and churn prevention is particularly crucial in the realm of insurance (high CAC, sticky contracts generating recurring revenue etc…). AI has a key role to play here, particularly to improve customer experience and customer success processes (i.e. dotData, Shift Technology, Integratz)

1.5 Claims Automation and Fraud Management

Claim Automation and Fraud Management are core, mission-critical operational activities for any insurance carrier and represent areas where insurers have already began to adopt AI (42% of insurers have already invested in Gen AI tools to combat fraud and manage claims) (TechNode Global).

Efficient claim management is a driving factor for customer satisfaction/retention, profitability, fraud risk mitigation, regulatory compliance and overall operational efficiency. Here as well, the potential impact of AI is immense given the highly time-consuming and data-driven nature of the task:

- Claims management technology: Predominantly platforms streamlining the entire claims lifecycle from “First Notice of Loss” (FNOL) to settlement using AI, analytics and automation. These platforms namely provide for automated workflows, enabling the automation of repetitive tasks such as document processing, claim routing and approvals to reduce manual efforts and processing time

- Fraud Management: AI has a crucial role to play when it comes to Fraud management and enables the following:

- Real-time Fraud Detection: Ability to analyze vast amounts of data in real-time allowing insurers to flag suspicious claims instantly

- Advanced Pattern Recognition: ML algorithms excel at identifying complex patterns and anomalies in claims data

- Predictive Analytics: Forecasting emerging fraud trends and anticipate potential spikes in fraudulent activity

- Document Authentication: Computer vision combined with AI can assist with the verification of submitted documents and detect signs of tampering or manipulation in various types of media (photos, videos, scanned files…)

- Behavioural Analysis: Monitoring and analysis of policyholder behaviour patterns across various touchpoints (i.e. social media, online activity…) to help identify inconsistencies

- False Positive Reduction: Improvement of AI models over time through iterative learning greatly reduces the rate of false positive alerts, ultimately allowing insurers to focus their resources on genuine fraud cases

Start-up Examples:

| Company Name | Description | HQ | Last Round | Total Raised ($M) | Invested Funds |

|---|---|---|---|---|---|

| Sprout.ai | Claim Automation | UK | Series A | 22 | Octopus, Amadeus Capital Partners, Portfolio Ventures |

| Applied AI | Claim Automation | UK | Series A | 45 | G42, A.R.M Holding |

| Captain | Claim Automation | USA | Series A | 107 | NFX |

| Tractable | Claim Automation | UK | Series E | 185 | Softbank, Insight Partners |

| Shift | Fraud Management | France | Series D | 315 | Bessemer Venture Partners, Mundi, Accel, General Catalyst |

| Roots Automation | Claim Automation | USA | Series B | 44 | CRV, Harbert Growth Partners |

1.6 Insurance Adjacents

Supporting infrastructure around insurance, highly tech-enabled but via commoditized technology. This mainly includes payment infrastructure, data collection hardware and data infrastructure software (toggle for more details). One could argue that many insurance adjacents need not be specific to the Insurance or Financial Services industry at all.

- Payment Infrastructure: Dedicated Fintech companies designed to modernize the flow of funds in the insurance industry

- Data Collection Hardware: Peripheral hardware (predominantly sensors and cameras) to monitor the usage and state of insured physical assets

- Data infrastructure: Horizontal data management platforms to set the right foundations for the implementation of AI (data centralization, cleaning, observability, manipulation and management)

2. B2B insurance opportunities

2.1 Cyber liability insurance

The cyber liability insurance market has undergone significant evolution since its inception in the 1990s, driven by technological advancements, regulatory changes, and the increasing frequency and severity of cyberattacks.

- Cyber insurance emerged in the late 1990s as a niche “specialty lines” product, initially designed to address risks like unauthorized system access, data loss, and online media errors. The first policy, launched in 1997 by AIG, focused on internet commerce risks and included both first- and third-party coverages (Source: Colony West)

- Early policies were limited in scope, often excluding key risks like rogue employees or regulatory fines. Coverage expanded in the 2000s to include business interruption, extortion, and network damage

- Regulatory developments such as California’s 2003 breach notification law and the EU’s GDPR in 2018 increased demand by mandating disclosure of data breaches. Insurers adapted by offering first-party coverages for breach-related costs like IT forensics and customer notifications

- The 2017 NotPetya attack marked a turning point, exposing the massive financial impact of cyberattacks. Coupled with the rise of ransomware attacks, insurers began tightening underwriting standards and raising premiums (Source: Jumpsec)

- By 2020, ransomware attacks had become a dominant threat. Loss ratios for insurers exceeded profitability thresholds, leading to stricter security requirements for policyholders and further premium increases

Market maturity – medium to high and growing:

- The global cyber insurance market grew from $7.8B in 2020 to $14B in 2023 and is projected to reach $29 billion by 2027. However, only a fraction of cyber risks are insured, with large companies dominating the market while SMEs remain underinsured (Source: Munich Re)

- Premiums have risen sharply—by over 94% from 2019 to 2022—due to escalating ransomware incidents. Insurers are now focusing on refining policy language to address ambiguities around state-sponsored attacks and other exclusions

- The market faces challenges such as high loss ratios (exceeding 60%), which threaten its sustainability. Insurers are increasingly cautious about pricing risks and setting coverage limits

- Despite these challenges, the market is expected to grow as businesses recognize the importance of mitigating financial losses from cyberattacks. Innovations in policy design aim to address evolving threats while balancing affordability for clients

The cyber liability insurance market has evolved from a niche product into a critical risk management tool. Its growth trajectory reflects rising awareness of cyber risks but also highlights ongoing challenges in balancing coverage needs with profitability. Any cyber tooling that can help insurers through bundling for prevention of losses or SaaS better pricing upfront could be of interest to Forestay, with scaled success stories in the space e.g. SecurityScorecard (US), CyberCube (US), Kovrr (Israel).

2.2 AI-related insurance

AI-related liability insurance is a specialized form of coverage designed to address risks and liabilities associated with the use, development, and deployment of artificial intelligence systems. It aims to provide protection against claims for damages caused by AI, such as bodily harm, financial loss, or intellectual property violations.

- Includes risks such as errors in AI decision-making, cybersecurity breaches, and software defects (Source: Commercial Risk Online)

- May cover professional liability (e.g., negligence in AI deployment), product liability (e.g., defective AI systems), and cyber liability (Source: Aon)

- The EU’s Artificial Intelligence Liability Directive (AILD) and Product Liability Directive are shaping the legal framework for AI-related claims, broadening the definition of products to include software and AI systems (Source: AI Liability Directive)

- These regulations are expected to influence mandatory insurance requirements for certain high-risk AI applications in the future

- Existing policies often lack clarity on whether AI-related incidents are covered, leading to “silent AI” coverage issues

- Insurers face difficulties in quantifying risks due to the complexity and novelty of AI systems

Market maturity – currently low with nascent potential, regulation could change this rapidly

- While traditional insurance policies (e.g., cyber or professional liability) address some AI risks, specific AI-focused insurance products are still in their infancy

- Large reinsurers like Munich Re have introduced tailored products for AI developers and adopters, while startups like Armilla AI offer performance guarantees for AI systems

- The insurance market is cautious, with few comprehensive solutions available. Many insurers remain in an observation phase due to regulatory uncertainty and evolving risk profiles

- As regulatory frameworks mature and insurers develop better actuarial models for AI risks, the market for AI-specific liability insurance is expected to grow significantly. This could include mandatory coverage for high-risk applications or stricter oversight of generative and autonomous AI technologies

While a dedicated market for AI-related liability insurance is emerging, it remains underdeveloped due to regulatory uncertainty and challenges in risk assessment. Existing policies often address these risks indirectly, but tailored solutions are gradually being introduced to meet the unique demands of this evolving field.

2.3 Embedded Insurance

Embedded insurance is the integration of insurance coverage directly into the purchase of non-insurance products or services, allowing consumers to access relevant insurance options seamlessly during their transaction journey. For example, customers can add travel insurance while booking a flight or purchase car insurance when buying a vehicle. This model eliminates the need for separate insurance shopping, making it more convenient and accessible for consumers. (Source: Insurtech Digital)

Market maturity – high with further potential

- The market was valued at $63.1B in 2022 and is projected to exceed $480B by 2033

- Some estimates suggest the potential market value could reach $3 trillion globally, indicating its transformative potential in the insurance industry (Source: IBM)

- For Insurers: Embedded insurance lowers distribution costs, improves customer acquisition, and enables access to real-time data for personalized offerings. It also expands the addressable market by tapping into new customer segments through partnerships with non-insurance entities

- For Businesses: Partnering with insurers allows businesses to offer added value to their products or services, improve customer retention, and generate additional revenue streams through profit-sharing models

- For Consumers: Embedded insurance provides convenience, affordability, and tailored coverage at the point of need, enhancing customer satisfaction and closing protection gaps

- Industries such as e-commerce, automotive, travel, and small business services are leading adopters of embedded insurance due to their ability to integrate digital solutions into their customer journeys

- Examples include Tesla offering its own vehicle insurance and Uber providing on-demand coverage for drivers (Source: One, Inc.)

The next phase of embedded insurance will likely warrant deeper integration with partners’ ecosystems to deliver seamless experiences, dynamic pricing, and innovative product bundling. Partnerships between insurers and non-insurance companies will continue to evolve, leveraging customer data to create unique and contextually relevant insurance solutions – the best enablers of embedded insurance could be Insurtech but may not appear to be “Insurtech” at face value e.g. applied Agentic AI.

2.4 Insurance-as-a-Service (IaaS)

Insurance-as-a-Service (IaaS) is a fully digital, cloud-based model that allows businesses to offer insurance products seamlessly through their platforms. It provides end-to-end solutions, including onboarding, claims management, customer support, and compliance, enabling companies to embed insurance into their offerings without building infrastructure from scratch. This approach is often referred to as “embedded insurance” and is designed to simplify the traditionally complex insurance process, making it more transparent and customer-centric. (Source: Qover)

Key features of IaaS include:

- Plug-and-play integration: Businesses can integrate pre-built insurance elements via APIs.

- Modular design: Tailored solutions for different industries and customer needs.

- Subscription-based model: Companies pay for services on a subscription basis, reducing costs and time-to-market (Source: Octamile)

- Market Opportunity – a subsegment of embedded insurance

- IaaS is a means of delivering Embedded Insurance (as discussed in 3.3)

- This model enhances customer experience by offering insurance at the point of sale (Source: Deloitte)

- The global insurance industry is undergoing digital transformation, with IaaS enabling faster go-to-market strategies and operational efficiencies

- In regions like the UK alone, the potential revenue disruption in the insurance market is estimated at £50B, highlighting opportunities for Insurtechs and incumbents alike (Source: PwC)

- Non-insurance companies can use IaaS to offer customized insurance products under their own brand, creating new revenue streams without significant investment

- Technologies like AI, blockchain, and cloud computing are enhancing underwriting, fraud detection, and customer service capabilities within IaaS platforms (Source: AI Multiple)

- These advancements allow insurers to meet evolving customer expectations while improving margins

Companies like Neodigital, Phoenix Group, and iptiQ are developing digital products that can be distributed and serviced by partners. Insurance-as-a-Service represents a transformative opportunity for these insurers and non-insurance businesses. Its scalability, cost-efficiency, and ability to meet modern consumer demands position it as a key driver of growth in the rapidly evolving insurance sector.

2.5 Telematics and parametrics-based commercial insurance

Leveraging IoT devices and big data analytics, insurers are offering more personalized and dynamic pricing models for commercial vehicles and fleet management, referred to as telematic insurance and for other use cases where the data collection can automatically trigger a potential insurance payout, referred to as parametric insurance.

Telematics insurance, also known as black box insurance, uses technology to track and record a policyholder’s driving behavior. It involves installing a GPS-based device in a vehicle or using a smartphone app to monitor various driving parameters such as speed, distance, location, braking, and cornering.

Key features of telematics insurance include:

- Usage-based pricing: Premiums are based on actual driving behavior and vehicle usage

- Risk assessment: Insurers can build more sophisticated risk models using collected data

- Personalized policies: Offers the potential for discounts and rewards for safe driving

The global insurance telematics market is experiencing rapid growth. It is projected to reach $18.7 billion by 2032, with a compound annual growth rate (CAGR) of 18.4% from 2024 to 2032 (Source: Insurtech Insights)

Parametric insurance is an agreement where the insurer pays a predetermined amount upon the occurrence of a specified event, such as an earthquake or hurricane of a certain intensity.

It uses objective parameters or indices to trigger payouts, rather than assessing actual losses. Key features of parametric insurance include:

- Index-based triggers: Payouts are based on predefined parameters like earthquake magnitude or wind speed

- Rapid payouts: Claims are processed quickly as they don’t require extensive loss assessment

- Customizable coverage: Parameters can be tailored to specific risks and needs

Parametric insurance is gaining traction as it can make insurance more accessible, affordable, and provide immediate payouts for individuals and businesses to recover quickly from losses.

The market opportunity for both telematics and parametric insurance is significant, driven by increasing demand for personalized insurance products, the need for more efficient claims processing, and advancements in technology and data analytics. These approaches are reshaping the insurance industry, offering new ways to assess risk, price policies, and provide coverage. There are multiple startups addressing parametric insurance, particularly in specialty lines (e.g. agribusiness, marine, weather and climate etc.) though quite fragmented by use case.

3. Conclusion

Insurance is unlikely to be fully disrupted—but it is being structurally reshaped. Deep-rooted legacy systems, regulatory constraints, and inherent risk aversion make rapid, end‑to‑end transformation unrealistic. Instead, innovation is concentrating where data density is high, economics are clear, and AI can deliver immediate, measurable impact.

Across the carrier value chain, pricing, underwriting, claims automation, and fraud management emerge as the most compelling adoption vectors. In these areas, AI directly improves loss ratios, speed, and customer satisfaction, making investment both defensible and urgent. Other functions—such as product development, operations, and distribution—are evolving more slowly, favouring incremental optimisation over radical change. As a result, successful Insurtechs are increasingly specialists rather than platforms: tightly scoped solutions that integrate with legacy environments and solve specific, high‑value problems.

On the B2B side, markets such as cyber insurance, AI-related liability, embedded insurance, and parametric models illustrate how insurance is being shaped by software, data, and context rather than traditional policy design. While maturity varies widely across these segments, the direction of travel is consistent: risk assessment and risk transfer are becoming more dynamic, data-driven, and embedded into broader digital workflows.

Ultimately, Insurtech’s next chapter is less about reinventing the insurance front‑end and more about quietly upgrading its engine. For incumbents, this means selective, AI-first modernisation. For startups and investors, the opportunity lies close to risk, data, and critical decision points—often in places that do not obviously “look” like insurance at first glance.

References and Resources:

- https://www.mapfre.com/media/The-State-of-Global-Insurtech_-By-Dealroom-Mundi-Ventures-and-MAPFRE.pdf

- https://www.pwc.ch/en/publications/2023/Insurtech-Deals-Market-Insights-EN-2023-web.pdf

- https://cdn.hl.com/pdf/2024/houlihan-lokey-2024-october-insurtech-report.pdf

- https://www.ajg.com/gallagherre/-/media/files/gallagher/gallagherre/news-and-insights/2024/november/global-insurtech-report-q3-2024.pdf

- https://technode.global/2025/01/24/how-ai-combats-business-insurance-fraud/